Obtain Life (and Living) Insurance for Your Family's Future...and Yours.

Providing a death benefit to protect your family is just the tip of the iceberg.

Equity Payments & Life helps you leverage life insurance to fast track your savings goals without risk.

Why You Should Consider Offering Indexed Universal Life Insurance (IUL) as an Alternative to 401(k) Plans? Read our Report ----->

Affordable Life (and Living)

Insurance, Retirement and Mortgage Protection and Income Options

What is Indexed Universal Life Insurance (IUL)?

An Indexed Universal Life (IUL) insurance policy combines the security of permanent life insurance with the potential for cash value growth linked to the positive performance and earnings of a major market index, such as the S&P 500®.

IULs provide the opportunity for the accumulation of cash value. The innovative design of an IUL not only ensures a death benefit for beneficiaries but also allows policyholders the potential to enhance their financial future by leveraging the positive movements of the stock market.

It's a strategic and customizable financial solution for those seeking permanent life insurance coverage with the added potential for long-term financial growth.

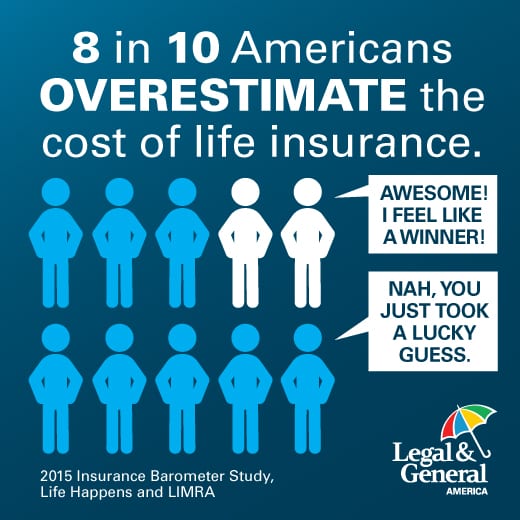

The most common reason people don’t have life insurance is that they think they cannot afford it. Among American adults, 32% to 47% believe life insurance is financially out of reach...on the contrary. Grab a Quote Today!!

Bonus Video: How Your Savings Grows In a IUL Insurance Policy

This video provides you with illustrations of different interest-saving scenarios; it will give you a great sense of the superiority of utilizing IUL policies to save your dollars over traditional savings bank accounts.

Final Expense Insurance

Final Expense Insurance is a type of whole life insurance policy with lower coverage amounts and more affordable premiums than other types of life insurance.

Final expense policies are designed to cover small to moderate costs, such as:

Funeral and burial arrangements; Medical bills; Nursing home expenses; Legal matters;

Travel costs; and Debts (like car payments, mortgages, or credit card balances).

Around 1 in 10 people who have life insurance don’t know what type of plan they have. Single people without children and working adults are the groups most likely to not understand their life insurance coverage, and as our lives change, so does our insurance needs change...and now, there are more options with more advantages. Grab a Quote!

Mortgage Protection Insurance from Americo

Help your family protect your mortgage payment in the event of your death. With our decreasing term life products, the death benefit is paid to your beneficiary in monthly income payments which may cover all or a portion of your mortgage payment.

This coverage also provides accelerated payouts should you experience critical, chronic, or terminal illness; optional disability income plans are also available. It can also provide an income to help take care of other financial obligations that your family may incur when you are gone.

Over the last 5-year period (as of 7/15/2024), the S & P 500 --the stock market index used to bear interest crediting to indexed universal life insurance policies -- has increased in value 86.85%; meanwhile, saving your money in a traditional savings bank account provides you an average annual return of 0.10%.

Click to fill out the form, select the 'Indexed Universal Life' Option and we will design an illustration much like the one featured in the bonus video above.

Term Life Insurance

Pays out a lump sum of money at the time of your death should it occur within the time your policy is in force (select from 10, 20, 25, and 30-year policy terms) and a claim has been submitted; in exchange, you pay a premium on a monthly, quarterly, or annual basis to keep the policy active.

Four Reasons Why We All Should Carry Life Insurance

To provide financial security to dependents:

Life insurance is designed to provide financial protection to your loved ones in the event of your death. If you have dependents such as children or elderly parents who rely on your income, life insurance can help ensure that they are taken care of financially even if you are no longer able to provide for them.To pay for final expenses:

In addition to providing financial support to your dependents, life insurance can also help cover the costs of your final expenses, such as funeral and burial expenses. These costs can be significant and can put a strain on your family's finances if they are not prepared to pay for them.To pay off debts and mortgages:

Life insurance can also be used to pay off any outstanding debts or mortgages that you may have. If you have a significant amount of debt, such as credit card debt or a mortgage, your death could leave your family with a significant financial burden. Life insurance can help pay off these debts so that your loved ones are not left with a financial burden.To supplement retirement income:

Life insurance can also be used as a retirement income supplement. If you have a permanent life insurance policy, you can borrow against the policy's cash value to supplement your retirement income. This can be particularly beneficial if you have not saved enough for retirement or if you want to maintain a certain standard of living in retirement.

We are the Life in

Equity Payments & Life...

As part of the award-winning Symmetry Financial Group,

Equity Life is contracted with top-rated life insurance companies across the country to serve individuals and families with affordable and customizable life insurance options that fit each budget. We leverage innovative insurance plans that can help you reach your savings and retirement goals, and can create generational wealth-building for all ages.

An agency family with licenses in all 50 states, providing a multitude of insurance options to fit every budget.

A quote and a free consultation is just a quick form fill away!

Equity Life, part of the Symmetry Financial Group

Licensed in all 50 States in the Union, contracted by over three-dozen top-rated life insurance companies, delivering a full-suite of life insurance, retirement, annuity and financial planning staples.

Frequently Asked Questions

What is Life Insurance?

Life insurance is a financial product that provides a lump sum payment to your beneficiaries upon your death, or in some cases, if you become permanently disabled or critically ill. It is designed to provide financial security to your loved ones in the event of your untimely death or illness.

But this is the tip of the iceberg: certain life insurance policies take a portion of your premiums and creates a cash value account that you can borrow from tax free. Policies that covers your income or mortgage payments if you become critically or terminally ill, and a host of other solutions that can be tailored to fits your budget and coverage needs.

What are the types of Life Insurance?

There are two main types of life insurance: term life insurance and permanent life insurance. Term life insurance provides coverage for a specific period of time, typically 10-30 years, while permanent life insurance provides coverage for the entirety of your life.

How much Life Insurance do I need?

The amount of life insurance you need depends on your individual circumstances, such as your income, debts, and dependents. As a general rule of thumb, financial experts suggest that you should have coverage that is at least 10-12 times your annual income.

How much does Life Insurance cost?

The cost of life insurance depends on various factors, such as your age, health, lifestyle, and the type of coverage you choose. Term life insurance is generally more affordable than permanent life insurance.

Is it necessary to have Life Insurance?

Life insurance is not legally required, but it can provide peace of mind and financial security for your loved ones in the event of your death or illness. If you have dependents who rely on your income, it may be especially important to consider life insurance.

Can I change my Life Insurance policy?

Yes, you can typically make changes to your life insurance policy, such as increasing or decreasing coverage, changing beneficiaries, or switching from one type of policy to another. However, these changes may be subject to certain restrictions or fees.

Do I need a medical exam to get Life Insurance?

It depends on the type of policy and the amount of coverage you are applying for. Term life insurance policies typically require a medical exam, while some permanent life insurance policies may not. However, your health and lifestyle may impact the cost of your coverage.

Can I name multiple beneficiaries on my Life Insurance policy?

Yes, you can name multiple beneficiaries on your life insurance policy and specify how the proceeds should be divided among them. You can also update your beneficiaries at any time if your circumstances change.

Large and Small Business Owners:

Avoid the costs of group life insurance.

We will be your staff's Life Insurance Broker.

Corporate Offices: 8 The Green, Suite A

Dover, Delaware, 19905

Call (951) 635-9407

Email: equitypayandlife@gmail.com